A roof hail damage insurance claim Texas homeowners file after a major storm can mean the difference between a fully restored property and thousands of dollars in unexpected expenses. Hailstorms strike quickly. The damage they leave behind can linger for years. That’s the challenge. Many property owners assume that if their roof isn’t leaking, everything is fine. Unfortunately, hail damage doesn’t always announce itself with obvious signs. Small impacts can weaken roofing materials, shorten the roof’s lifespan, and create hidden vulnerabilities that eventually lead to expensive repairs.

I’ve seen homeowners discover major issues months after a storm because the initial damage appeared minor. By then, proving the connection to the storm became much more difficult. The good news? You can protect your roof, strengthen your insurance claim, and improve your chances of receiving a fair settlement if you know what to look for and what steps to take. This guide walks through the entire process. We’ll cover how to identify hail damage, document losses, navigate insurance inspections, understand supplements, and learn why professional representation often changes claim outcomes.

Understanding Hail Damage and Why It Matters

Hail may look harmless once it lands on the ground. The reality is very different. When hailstones fall from thousands of feet in the atmosphere, they can reach speeds capable of damaging roofing systems, gutters, siding, windows, and exterior structures.

The severity of damage depends on several factors:

- Hail size

- Wind speed

- Roof age

- Roofing material

- Impact angle

- Storm duration

A one-inch hailstone striking an aging roof can sometimes cause more damage than a larger hailstone hitting a newer roof. That’s why every storm should be evaluated individually.

Common Signs of Roof Hail Damage

Many indicators can be identified from the ground, while others require a closer inspection.

Look for:

- Missing granules in gutters

- Dented gutters and downspouts

- Damaged roof vents

- Cracked skylights

- Metal flashing dents

- Shingle bruising

- Broken tiles

Some signs appear immediately. Others take months to develop.

Why Small Damage Becomes a Big Problem

One hail impact rarely destroys a roof. However, dozens or hundreds of impacts can gradually compromise roofing materials.

Over time, this may lead to:

| Potential Issue | Long-Term Effect |

| Granule loss | Accelerated aging |

| Cracked shingles | Water penetration |

| Damaged flashing | Leaks around roof openings |

| Broken tiles | Underlayment exposure |

| Moisture intrusion | Mold growth |

The earlier damage is documented, the stronger your position becomes when pursuing a hail damage on roof insurance claim.

How to Identify Hail Damage by Roof Type

Not all roofs respond to hail the same way. This is where roofing expertise becomes critical. A damage pattern that indicates a covered loss on one roof may not look the same on another.

Asphalt Shingle Roof Hail Damage

Asphalt shingles are among the most common roofing materials in Texas. They’re also highly susceptible to hail impacts.

Typical indicators include:

- Circular impact marks

- Granule displacement

- Dark spots where granules are missing

- Soft bruised areas

- Fractured fiberglass matting

Inspectors often test suspicious areas by gently pressing on impact points. A damaged shingle frequently feels soft compared to surrounding material.

Metal Roof Hail Damage

Metal roofs create unique claim challenges. Some dents affect appearance only. Others affect functionality.

Insurance carriers often distinguish between:

Cosmetic Damage

- Minor denting

- Surface blemishes

- Visual imperfections

Functional Damage

- Seam damage

- Panel punctures

- Fastener failures

- Water intrusion vulnerabilities

Functional damage typically carries greater significance during a hail roof damage insurance evaluation.

Tile Roof Hail Damage

Tile roofing systems require particularly careful inspections.

Clay and concrete tiles can:

- Crack

- Fracture

- Chip

- Break internally

Internal fractures often remain hidden until tiles are lifted. This is why surface-level inspections sometimes fail to reveal the full extent of damage.

Flat and Commercial Roofing Systems

Commercial properties face different risks.

Common damage includes:

- Membrane punctures

- Seam separation

- Insulation compression

- Coating damage

- HVAC impact damage

Even small punctures can allow moisture to infiltrate insulation layers. Once trapped, moisture may spread far beyond the original impact area.

Why Professional Inspections Matter

Homeowners should never feel pressured to climb onto a roof after a storm.

Besides safety concerns, many forms of hail damage require specialized training to identify accurately.

A professional inspection can:

- Locate hidden impacts

- Differentiate hail damage from wear and tear

- Create photographic evidence

- Support future claim negotiations

This documentation becomes essential during a roof hail damage insurance claim Texas process.

Immediate Steps to Take After a Hailstorm

What you do in the first few days matters. A lot. Mistakes made immediately after a storm can complicate claims for months.

Prioritize Safety First

Safety comes before documentation. Always.

Avoid:

- Climbing on damaged roofs

- Walking near unstable structures

- Entering unsafe attic spaces

- Touching damaged electrical components

Wait until conditions are safe.

Conduct a Ground-Level Inspection

You can often identify valuable evidence without leaving the ground.

Check:

- Gutters

- Downspouts

- Siding

- Window screens

- Outdoor furniture

- Air conditioning units

Dents on soft metals frequently provide strong evidence that hail impacted the property.

Prevent Additional Damage

Insurance policies generally require policyholders to mitigate further damage.

Reasonable temporary measures may include:

- Tarping openings

- Removing water

- Protecting contents

- Securing exposed areas

Keep every receipt. Save every invoice. These expenses may become reimbursable.

Notify Your Insurance Company

Prompt reporting helps establish a clear timeline.

When opening a claim:

- Record claim numbers

- Save adjuster contact information

- Document every conversation

- Request written confirmations whenever possible

Organization becomes your ally.

Schedule a Professional Roof Inspection

Independent evaluations often uncover issues that homeowners miss.

The inspection report should include:

- Photographs

- Measurements

- Damage descriptions

- Roof condition notes

- Repair recommendations

This information strengthens any future hail damage on roof insurance claim.

Roof Hail Damage Insurance Claim Texas: How the Process Works

Many homeowners file only one or two property claims in their lifetime. As a result, the process can feel unfamiliar. Understanding the steps removes uncertainty.

Filing the Initial Claim

The process typically begins with:

- Reporting the loss

- Providing storm details

- Sharing property information

- Scheduling an inspection

The insurance carrier assigns a claim representative who coordinates the next stages.

The Insurance Inspection

During the inspection, adjusters generally evaluate:

- Roofing materials

- Gutters

- Flashing

- Vents

- Exterior elevations

- Ancillary structures

Take notes. Ask questions. Request clarification whenever necessary.

Reviewing the Scope of Loss

After inspection, the carrier typically prepares a scope of loss.

This document outlines:

- Covered damage

- Approved repairs

- Pricing

- Material quantities

Many homeowners focus only on the settlement amount. The scope itself often deserves greater attention. Why? Because missing items frequently originate in the scope, not necessarily the payment amount.

Understanding Your Policy Coverage

Several policy provisions influence settlement outcomes.

Replacement Cost Value (RCV)

Pays the cost of replacing damaged property, subject to policy terms.

Actual Cash Value (ACV)

Accounts for depreciation. Older roofs often receive reduced initial payments under ACV calculations.

Deductibles

The amount the policyholder contributes before coverage applies.

Exclusions

Certain causes of loss may be excluded or limited. Always review policy language carefully before accepting claim conclusions.

How to Document Damage for a Strong Claim

Documentation wins claims. Not opinions. Not assumptions. Evidence. The more organized your documentation, the easier it becomes to support your position. One of the most valuable skills a homeowner can develop after a storm is understanding How to Document Hail Damage for an Insurance Claim. Detailed photographs, inspection reports, weather data, contractor assessments, and organized claim records can significantly strengthen a roof hail damage insurance claim Texas and reduce the likelihood of disputes later in the process.

Take Comprehensive Photographs

Capture both broad and detailed views.

Photograph:

- Entire roof slopes

- Individual impact marks

- Gutters

- Flashing

- Vents

- Skylights

- Interior water damage

Take photos before temporary repairs whenever possible.

Create a Damage Inventory

Build a written inventory that includes:

| Property Component | Observed Damage |

| Roof | Impact marks |

| Gutters | Denting |

| Siding | Surface impacts |

| Windows | Cracking |

| HVAC Units | Fin damage |

A detailed inventory prevents important items from being overlooked.

Gather Supporting Evidence

Strong claims often include:

- Weather reports

- Radar data

- Contractor reports

- Inspection findings

- Prior maintenance records

Multiple sources of evidence create a stronger narrative. Accurate documentation is often the difference between a straightforward claim and a prolonged dispute. In many technical fields, professionals rely on systematic methods of collecting and analyzing information. A good example is Bayesian inference, which involves updating conclusions as new evidence becomes available. While roofing claims are very different, the principle is similar: the more credible evidence you gather, the stronger your position becomes when supporting a roof hail damage insurance claim Texas.

Maintain a Claim File

Keep everything together.

Store:

- Emails

- Inspection reports

- Estimates

- Photographs

- Claim correspondence

- Receipts

An organized claim file can significantly improve outcomes when disputes arise later in the process. For homeowners in Cameron and throughout Texas, thorough documentation often becomes the foundation of a successful roof hail damage insurance claim Texas settlement.

What Insurance Carriers Commonly Miss in Their Scope

One of the biggest misconceptions homeowners have is that the first insurance estimate is always complete. It often isn’t. Most adjusters work hard and genuinely try to document damage accurately. However, time constraints, weather conditions, roof complexity, staffing shortages, and simple oversight can lead to omissions. Those omissions matter. A missing item here. An underestimated quantity there. Suddenly, a property owner is facing thousands of dollars in uncovered repair costs. Understanding what commonly gets overlooked can help you identify gaps before repairs begin.

Roofing Components Beyond Shingles

Many claim estimates focus heavily on shingles. The problem? A complete roofing system includes far more than shingles alone.

Commonly missed roofing materials include:

- Starter shingles

- Ridge cap shingles

- Hip cap materials

- Drip edge

- Ice and water barriers

- Roofing felt

- Synthetic underlayment

Each component serves a purpose. If damaged materials are not included in the scope, contractors may be forced to request additional funding later.

Flashing Components

Flashing is critical. And it is frequently overlooked. Flashing helps direct water away from vulnerable areas where roofing materials meet penetrations or transitions.

Common flashing components include:

- Pipe jack flashing

- Step flashing

- Valley flashing

- Counter flashing

- Chimney flashing

Each component contributes to water protection. Each should be evaluated carefully. When flashing damage goes unnoticed, future leaks often follow.

Ventilation Systems

Roof ventilation is another area where omissions occur.

Ventilation systems often include:

- Ridge vents

- Static vents

- Turbine vents

- Intake vents

- Power vents

Many of these components are made from metal or plastic materials that can sustain hail impacts. A proper hail roof damage insurance evaluation should examine every ventilation component on the roof.

Code Upgrade Requirements

Building codes change. Insurance scopes sometimes fail to account for those changes.

Common code-related expenses include:

| Code Upgrade Item | Potential Cost Impact |

| Ice barrier requirements | Additional materials |

| Ventilation improvements | Additional labor |

| Fastener upgrades | Increased installation costs |

| Deck attachment requirements | Structural expenses |

| Permit compliance | Administrative costs |

Many policies contain Ordinance and Law coverage that may help address these expenses. However, code upgrades often require proper documentation before carriers approve payment.

Hidden Damage Beneath Roofing Materials

This is where many disputes begin. Some forms of hail damage simply cannot be seen during an initial inspection.

Examples include:

- Damaged underlayment

- Saturated insulation

- Decking deterioration

- Fastener failures

- Moisture intrusion

These issues often appear only after roofing materials are removed. That doesn’t make them less real. It simply means additional documentation becomes necessary.

Access and Safety Requirements

Not every roof is easy to inspect.

Factors that complicate inspections include:

- Steep slopes

- Multiple roof levels

- Limited access points

- Safety concerns

- Weather conditions

Certain areas may not receive the same level of evaluation as others. As a result, portions of damage may remain undocumented during the first inspection. This is one reason supplements are so common in a roof hail damage insurance claim Texas. Many initial insurance estimates are based only on damage visible during the first inspection. However, roofing projects frequently uncover additional issues such as damaged flashing, underlayment deterioration, ventilation upgrades, code compliance requirements, and decking damage. This is why Hail Damage Claim Supplements: What Carriers Miss in Their Scope has become such an important topic for Texas property owners. Supplements allow policyholders to seek additional compensation for legitimate repair costs that were not identified during the original inspection.

Hail Damage Claim Supplements

Many homeowners hear the word “supplement” and assume something went wrong. Actually, supplements are common. Very common.

What Is a Supplement?

A supplement is a request for additional claim funding based on newly identified or previously undocumented damage. Think of it this way. The original estimate reflects what was known during the initial inspection. The supplement reflects what became known afterward. Supplements help bridge the gap between the original scope and the actual repair requirements.

Why Supplements Become Necessary

Several factors can trigger supplemental requests.

These include:

- Hidden damage discovery

- Code compliance requirements

- Material availability issues

- Quantity adjustments

- Roofing system complexity

- Additional labor requirements

None of these situations are unusual. In fact, they occur regularly during large storm events.

The Supplement Process Step by Step

Step One: Additional Damage Is Identified A contractor, consultant, or public adjuster discovers damage that was not included in the original estimate.

Step Two: Documentation Is Gathered

Supporting documentation may include:

- Photographs

- Measurements

- Contractor reports

- Manufacturer specifications

- Building code references

Documentation drives the process. Without it, approval becomes difficult.

Step Three: Supplement Submission

The supporting materials are submitted to the insurance carrier for review. Clear organization matters. The easier the information is to understand, the easier it becomes to evaluate.

Step Four: Carrier Review

The carrier reviews the submitted information and determines whether additional payment is warranted. This stage often involves questions, requests for clarification, or additional inspections.

Step Five: Approval and Payment

Once approved, additional funds are issued to cover documented damages.

Why Accurate Supplements Matter

Supplements are not about inflating claims.

They’re about accuracy.

A properly documented supplement can help ensure that:

- Roofing systems are restored correctly

- Code requirements are met

- Contractors have adequate funding

- Homeowners avoid unexpected expenses

For many policyholders, supplements become one of the most important aspects of a successful hail damage on roof insurance claim.

Public Adjuster vs. Insurance Adjuster for Hail Claims

This topic creates confusion. The titles sound similar. The responsibilities are very different. Understanding those differences can significantly affect claim outcomes.

Who Works for the Insurance Company?

Insurance carriers may assign:

Staff Adjusters

Employees of the insurance company.

Independent Adjusters

Contracted professionals hired by the carrier. Both evaluate claims on behalf of the insurer. Their role is to inspect damage, review coverage, and prepare estimates according to carrier guidelines.

What Does a Public Adjuster Do?

A public adjuster works for the policyholder.

Not the insurance company.

Their responsibilities may include:

- Policy analysis

- Damage assessment

- Documentation review

- Claim preparation

- Negotiation support

- Supplement coordination

Their objective is to ensure covered damage is fully documented and properly evaluated.

Many homeowners are unfamiliar with the differences between claim professionals, which makes understanding Public Adjuster vs. Insurance Adjuster for Hail Claims in Cameron, TX especially important. While insurance adjusters evaluate claims on behalf of the carrier, public adjusters represent policyholders and help document, prepare, and negotiate covered damages throughout the claim process.

Key Differences Homeowners Should Understand

| Public Adjuster | Insurance Adjuster |

| Represents policyholder | Represents insurer |

| Reviews policyholder interests | Reviews carrier obligations |

| Documents damages comprehensively | Evaluates reported damages |

| Negotiates on behalf of homeowner | Evaluates claim based on coverage |

| Assists with supplements | Reviews supplement requests |

Neither role is inherently adversarial. However, understanding who each professional represents is important.

Why This Distinction Matters

When significant hail damage exists, claim complexity increases. The larger the loss, the more important documentation becomes.

Professional representation often helps homeowners:

- Understand policy language

- Identify overlooked damages

- Navigate disputes

- Organize claim evidence

Those benefits can become especially valuable during a roof hail damage insurance claim Texas.

Why a Public Adjuster Often Changes the Outcome

Every claim is different. Not every claim requires professional representation. However, there are situations where a public adjuster can dramatically improve the process.

More Thorough Damage Documentation

Documentation drives claim outcomes.

Public adjusters typically spend substantial time evaluating:

- Roofing materials

- Flashing systems

- Ventilation components

- Ancillary structures

- Interior damages

Their inspections are often far more detailed than homeowners expect.

Better Claim Presentation

Evidence matters. Presentation matters too. Well-organized claims generally receive faster and more efficient review.

Professional claim packages often include:

- Damage narratives

- Photographic evidence

- Measurement reports

- Policy references

- Supporting estimates

The goal is clarity.

Stronger Supplement Negotiations

Supplements succeed when supported by evidence.

Public adjusters frequently assist with:

- Scope comparisons

- Documentation review

- Additional inspections

- Code compliance analysis

This level of support can help ensure legitimate damages receive appropriate consideration.

Reduced Stress for Property Owners

Storm recovery is stressful. There’s no way around that. Managing inspections, contractors, adjusters, emails, estimates, and documentation can quickly become overwhelming. Many homeowners value professional assistance simply because it allows them to focus on family, work, and recovery.

Real-World Benefits for Homeowners

Property owners face the same challenges seen across Texas. Severe weather can arrive with little warning. Roof systems can sustain damage that is not immediately visible. Professional claim support can help identify issues before they become larger problems. For many homeowners, that peace of mind alone provides significant value.

Common Mistakes That Can Hurt Your Claim

Even legitimate claims can encounter difficulties when avoidable mistakes occur. Fortunately, most of these mistakes are preventable.

Waiting Too Long to File

Time matters. The longer damage goes unreported, the more difficult it can become to establish a clear connection between the storm and the loss. Prompt reporting strengthens credibility.

Failing to Document Damage

Photos disappear. Evidence fades. Repairs happen. Documentation should begin as soon as conditions are safe.

Making Permanent Repairs Too Soon

Emergency mitigation is important. Permanent repairs before inspection can create complications. Whenever possible, document conditions thoroughly before major work begins.

Throwing Away Damaged Materials

Damaged shingles, flashing, vents, and other components may serve as evidence later. Preserve materials whenever practical.

Accepting the First Settlement Without Review

Many homeowners assume the initial estimate is final. Often, it is not. Carefully review the scope before authorizing repairs.

Missing Supplement Opportunities

Hidden damage is common. Code upgrades are common. Scope revisions are common. Ignoring supplement opportunities may leave money on the table and increase out-of-pocket expenses. When pursuing a hail roof damage insurance claim, thorough review remains one of the most effective ways to protect your interests.

Protecting Your Roof Before the Next Hailstorm

You can’t stop hail. You can, however, reduce the damage it causes. Many homeowners focus on insurance only after a storm hits. The smarter approach is preparing long before severe weather arrives. A well-maintained roof is generally easier to inspect, easier to document, and easier to repair after a storm.

Schedule Regular Roof Inspections

Routine inspections help identify existing issues before hail damage occurs. Why is that important? Because insurance carriers often distinguish between storm damage and pre-existing wear and tear. If a roof already has significant deterioration, claim evaluations can become more complicated. A professional inspection every year or after major storms can provide valuable documentation of your roof’s condition.

Inspection reports should include:

- Photographs

- Material condition assessments

- Ventilation evaluations

- Flashing inspections

- Maintenance recommendations

These records may become useful evidence later.

Keep Gutters and Drainage Systems Clean

Clogged gutters can worsen storm-related damage. Water that cannot drain properly may back up beneath roofing materials, increasing the risk of leaks and moisture intrusion.

At a minimum:

- Remove leaves and debris regularly

- Check downspouts for blockages

- Inspect gutter fasteners

- Replace damaged sections promptly

Small maintenance tasks today can prevent large repair bills tomorrow.

Address Minor Repairs Quickly

A cracked shingle may not seem urgent. A loose flashing component may appear insignificant. Yet those small defects can become weak points during severe weather. Timely repairs help maintain the integrity of the roofing system and reduce the likelihood of additional storm-related damage.

Consider Impact-Resistant Roofing Materials

Some roofing products are designed specifically to withstand hail impacts better than standard materials.

Potential options include:

| Roofing Material | Hail Resistance |

| Standard asphalt shingles | Moderate |

| Impact-resistant shingles | High |

| Standing seam metal roofing | High |

| Concrete tile | Moderate to High |

| Synthetic roofing products | High |

Not every property requires an upgrade. However, homeowners living in hail-prone regions may benefit from discussing impact-resistant options with a qualified roofing professional.

Maintain Property Records

Documentation shouldn’t begin after a storm.

It should already exist.

Keep records of:

- Roof installation dates

- Prior repairs

- Inspection reports

- Contractor invoices

- Warranty information

When a roof hail damage insurance claim Texas arises, organized records can help establish the roof’s condition before the storm occurred.

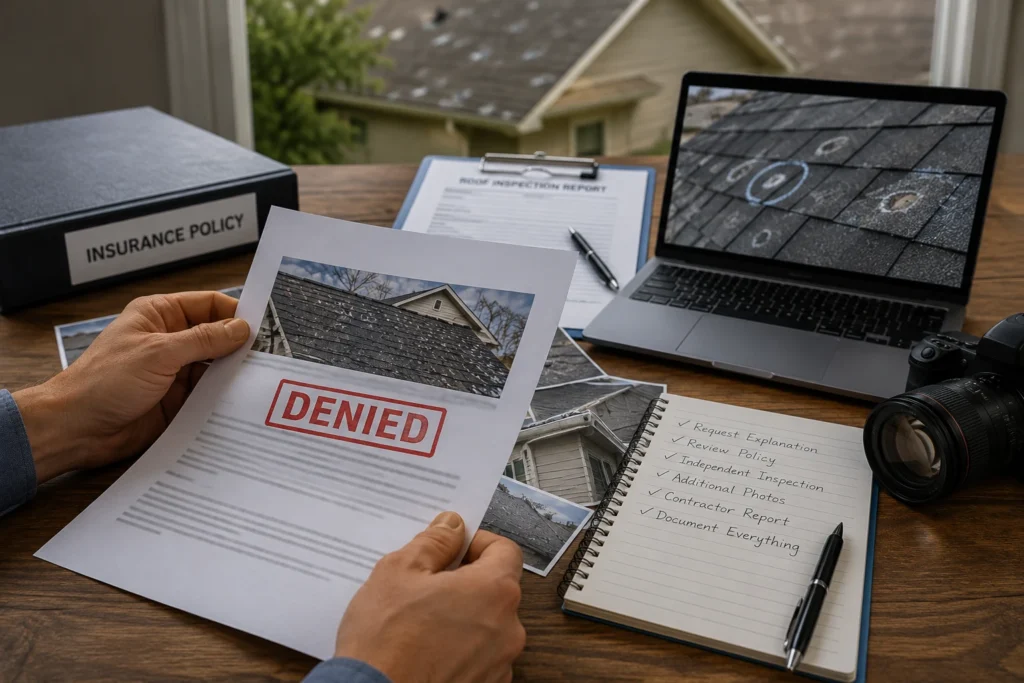

When a Hail Claim Is Denied

Claim denials can be frustrating. After documenting damage, meeting with inspectors, and waiting for a decision, receiving a denial letter can feel like a major setback. However, a denial does not always mean the matter is closed. Many claims are successfully reconsidered when additional evidence becomes available. Understanding What to Do If Your Hail Claim Was Denied in Cameron, TX can help homeowners respond strategically rather than emotionally. Reviewing the denial letter carefully, obtaining an independent roof inspection, gathering supplemental documentation, and comparing the findings against policy language can often reveal opportunities to challenge an unfavorable decision.

Common Reasons Claims Are Denied

Insurance carriers may deny claims for several reasons, including:

- Insufficient evidence of storm damage

- Pre-existing roof deterioration

- Wear and tear exclusions

- Late reporting

- Coverage limitations

- Disputed cause of loss

A denial should always be reviewed carefully before accepting the outcome.

Steps to Take After a Denial

If your claim is denied, consider the following actions:

- Request a detailed explanation

- Review your insurance policy

- Obtain an independent inspection

- Gather additional photographs

- Secure contractor reports

- Document any overlooked damage

The more evidence you can provide, the stronger your position may become during reconsideration discussions.

Seek Professional Guidance When Necessary

Some denied claims involve complex policy language, conflicting inspections, or disputed damage assessments. In those situations, professional assistance may help clarify the available options and improve claim organization moving forward.

Why Homeowners in Cameron Should Act Quickly After Hail Damage

After a major hailstorm, many homeowners adopt a wait-and-see approach. Sometimes that works. Often it doesn’t. The problem is that hail damage rarely improves with time. It typically becomes worse.

Hidden Damage Doesn’t Stay Hidden Forever

A roof may appear intact immediately after a storm. Yet beneath the surface, impacts may have compromised shingles, flashing, underlayment, or tile systems.

Months later, homeowners begin noticing:

- Ceiling stains

- Interior leaks

- Mold growth

- Increased energy costs

- Premature roof deterioration

By then, proving the relationship between the storm and the damage may become more difficult.

Insurance Deadlines Matter

Every policy contains reporting requirements. While specific deadlines vary, delayed reporting can create unnecessary complications.

Prompt action helps:

- Preserve evidence

- Strengthen documentation

- Improve claim efficiency

- Reduce disputes

The sooner damage is evaluated, the stronger the foundation of the claim becomes. Contractors Become Busier After Major Storms Following significant hail events, roofing contractors often experience substantial increases in demand. Inspection schedules fill quickly. Repair schedules become longer. Material availability can tighten. Homeowners who act promptly often gain access to inspections and repairs sooner than those who wait.

Early Documentation Creates Leverage

Documentation collected immediately after a storm is often the most persuasive.

Fresh evidence may include:

- Impact photographs

- Weather reports

- Hail measurements

- Property condition records

As time passes, evidence can disappear. That’s why immediate action frequently produces stronger outcomes during a hail damage on roof insurance claim.

Building a Strong Claim From Day One

The most successful claims generally follow a similar pattern.

Property owners:

- Act quickly

- Document thoroughly

- Stay organized

- Understand their policy

- Review the scope carefully

- Pursue supplements when justified

None of these steps guarantee a specific outcome. However, together they create a significantly stronger claim file.

A Simple Claim Checklist

After a hailstorm:

✓ Ensure everyone is safe

✓ Conduct a ground-level inspection

✓ Photograph visible damage

✓ Contact your insurance company

✓ Schedule a professional roof inspection

✓ Create a claim file

✓ Save receipts and invoices

✓ Review the insurance scope carefully

✓ Document additional damage discovered during repairs

✓ Consider professional claim assistance when necessary

This checklist alone can help homeowners avoid many of the most common claim pitfalls.

The Financial Impact of an Incomplete Claim

Many homeowners focus only on obtaining claim approval. Approval is important. Completeness is equally important. A partially documented claim can leave property owners responsible for expenses that should have been included from the beginning.

Potential overlooked costs may involve:

- Roofing accessories

- Flashing replacement

- Ventilation upgrades

- Code compliance requirements

- Safety equipment costs

- Additional labor requirements

Even small omissions can add up quickly. That’s why reviewing the scope line by line remains one of the most valuable steps in the process. A successful hail roof damage insurance claim is not simply about receiving payment. It’s about receiving enough funding to restore the property properly.

Why Thorough Documentation Remains the Most Powerful Tool

If there is one lesson homeowners should remember, it’s this: Documentation wins. Not assumptions. Not opinions. Not guesses. Documentation.

The strongest claims typically include:

- Clear photographs

- Inspection reports

- Weather data

- Contractor assessments

- Detailed estimates

- Organized correspondence

Evidence transforms a claim from a discussion into a documented file supported by facts. That distinction often becomes critical during disputes or supplement negotiations.

Conclusion

A hailstorm can last only a few minutes. The effects can linger for years. That’s why understanding the roof hail damage insurance claim Texas process is so important for property owners. From identifying damage by roof type to documenting losses, reviewing insurance scopes, and navigating supplements, every step plays a role in the final outcome.

The most successful claims rarely happen by accident. They result from preparation, organization, and careful attention to detail. Whether your roof consists of asphalt shingles, metal panels, tile, or a commercial roofing system, early action remains one of the best ways to protect your investment. Thorough inspections, detailed documentation, and a clear understanding of policy coverage can significantly improve the claim experience.

For homeowners in Cameron and throughout Texas, hailstorms are an unfortunate reality. Fortunately, property owners have options. By acting quickly, preserving evidence, reviewing claim documentation carefully, and understanding what carriers commonly miss, you can place yourself in a stronger position when pursuing a roof hail damage insurance claim Texas. When significant damage exists, professional assistance may also help uncover overlooked items, support supplements, and improve claim organization. Every property is different. Every storm is different. However, one principle remains consistent. The better the documentation, the stronger the claim. Protect your roof. Protect your evidence. Protect your financial recovery. Those steps can make all the difference when the next hailstorm arrives.

FAQs

Look for missing granules, dented metal components, cracked tiles, or bruised shingles. A professional inspection can identify hidden damage that may not be visible from the ground.

You should report the damage as soon as possible after the storm. Prompt reporting helps preserve evidence and avoids potential issues with claim deadlines.

Coverage depends on your policy, the extent of damage, and whether replacement is warranted. Review your policy carefully to understand deductibles, exclusions, and settlement terms.

Keep photographs, inspection reports, repair estimates, receipts, weather reports, and all communications with your insurance company.

Yes. Hail impacts can weaken roofing materials and flashing, allowing water intrusion to develop long after the storm has passed.

A supplement is a request for additional funds when hidden damage or overlooked repair items are discovered after the initial claim estimate is prepared.

Initial inspections may not reveal hidden damage beneath roofing materials, and some roofing components can be overlooked during the first evaluation.

Only temporary emergency repairs should be completed before the inspection. Always document the damage thoroughly before performing permanent repairs.

In some cases, yes. New evidence, independent inspections, and additional documentation may support reconsideration of a denied claim.

A public adjuster represents the policyholder by documenting damages, reviewing policy coverage, preparing claim information, and assisting with negotiations.